[ad_1]

A behavioral change mannequin profitable in selling more healthy behaviors and efficiently carried out in all of the continents —

By Matteo Carbone, Founder & Director, IoT Insurance coverage Observatory —

About 30 years in the past, Adrian Gore and Barry Swartzberg harbored an instinct that launched a unique perspective on folks’s well-being. This strategy, often known as Vitality, has since matured into a technique primed to function a basic competency for any insurer sooner or later. The insurance coverage sector has wholeheartedly embraced the notion of incorporating preventive measures, as aptly expounded in The Geneva Affiliation’s publication titled “From Risk Transfer to Risk Prevention.” The crucial to domesticate much less dangerous behaviors amongst policyholders in private traces and amongst frontline staff in business domains stands because the indispensable path in direction of realizing this aspiration.

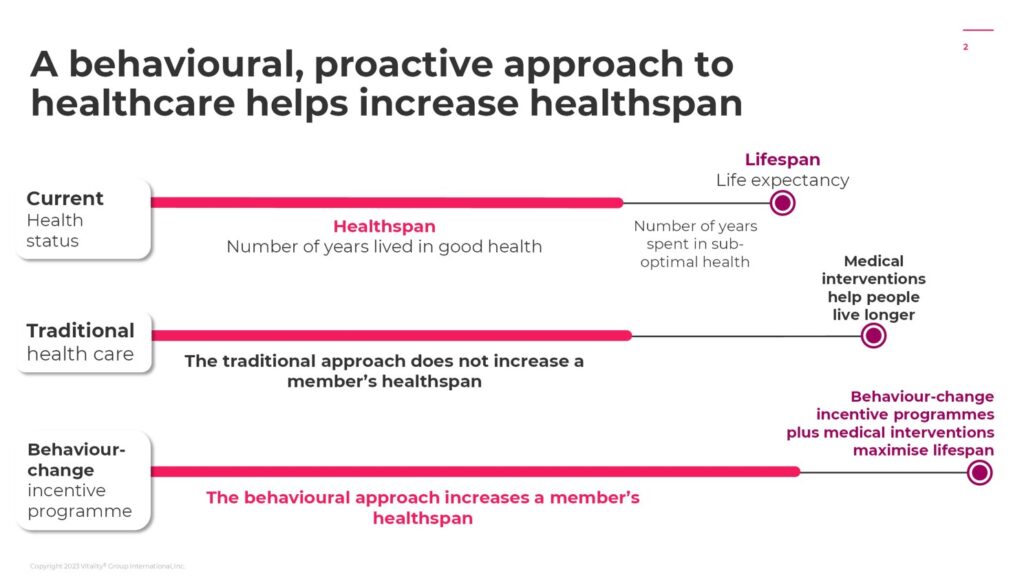

The traditional medical standpoint primarily facilities upon using medical interventions as soon as a illness has manifested. In essence, this strategy entails prolonging life by extending the interval spent in considerably suboptimal well being, albeit with variations contingent upon the character of the illness. Conversely, Vitality’s behavioral paradigm concentrates on selling more healthy life-style decisions able to elongating the length of the policyholder’s time spent in a state of optimum well-being, thus additional extending their lifespan.

A behavioral, proactive strategy to healthcare (Supply: Discovery)

Realizing these outcomes entails diminishing the frequency and severity of claims for the insurer. This incremental financial worth is then partially channeled towards funding the bills of the behavioral change program. At its core, the Vitality program includes – after adequately underwriting a danger – promising rewards to people exhibiting enhancements of their conduct. This, in flip, garners insurer’s enhanced technical outcomes from these shifts in life-style decisions. A portion of those financial upsides is allotted to upholding these guarantees.

Over the previous decade, this strategy has been replicated in several markets – with completely different nuances program by program, and even one of many worldwide companions has used Vitality as a stand-alone fee-based provide open to clients with none insurer coverage – and has already attracted greater than over 30 million[1] people globally. This journey has showcased an astonishing capability to actively interact policyholders. Throughout quite a few Vitality portfolios, a substantial majority of the members, exceeding two-thirds[2], have engaged in each bodily and non-physical actions offering verified info. These days, greater than 100K new units per thirty days[3] are linked by members to the Vitality program.

Discovery has completed an enrollment charge starting from 50% to 80% of their Vitality program amongst their South African policyholders. This exceptional achievement has been realized even with a month-to-month charge exceeding $17[4] charged to the insured for enrollment.

The worldwide partnerships are yielding constant proof as nicely, demonstrating penetration charges of as much as 70%[5] for Vitality in companions’ new enterprise applications deployed in mature nations – even with a charge requested to policyholders to hitch this system and about 5 years available on the market – and as much as 80% in rising economies[6]. Analogous outcomes have been replicated in company wellness initiatives, the place as a lot as two-thirds of eligible staff have participated, in distinction to the trade’s common of 30% participation.

This engenders a virtuous cycle whereby policyholders crave to share their wholesome behaviors with their insures and revel in substantial benefits, with advantages that that the advantages could be increased than the premium paid. Concurrently, this Shared-Worth Insurance coverage mannequin permits the provider to attain superior outcomes, thereby producing noteworthy constructive externalities for society at massive.

The inspiration of the Vitality strategy resides in selling behaviors immediately contributing to delaying ailments. Discovery’s three-decade journey supplies sturdy proof {that a} vital improve within the stage of bodily exercise reduces by 49% the mortality for people aged 45 to 65, and a exceptional 61% discount for these older.[7] Optimistic impacts have additional manifested inside annual medical expenditures, the place probably the most engaged members 15% decrease declare price[8] than the much less engaged, risk-adjusted by age and medical situations. A longitudinal research on the individuals who confirmed a low stage of bodily exercise through the preliminary six-month interval confirmed a subsequent 14% discount in-hospital medical prices for the subgroup that notably elevated their engagement ranges over the following 4 and a half years.[9]

Mortality advantages from change in train (Supply: Discovery)

As intuitively anticipated a program encouraging wholesome behaviors and incentivizing people showcasing such conduct inherently possesses additionally the potential to draw and retain extra folks with a wholesome life-style. In an illustration of this impact, Discovery’s newest information pertaining to their SA well being portfolio confirmed that the financial worth the insurer garners by way of the Vitality strategy is derived to the extent of 31% from the attraction and retention of youthful members, and 20% from the attraction of people extra prone to train. Consequently, almost half of the accrued financial worth could be attributed to conduct change—an elevated stage surpassing the 28% recorded in 2016.[10]

The enhancement evident within the attained outcomes is a direct end result of Discovery’s steady innovation effort. This ongoing endeavor has constantly honed their mastery in behavioral modification, seamlessly making use of it throughout varied geographical areas and contours of enterprise. As illustrated by the determine beneath, the dynamic utilization of Lively Rewards and loss aversion mechanisms (such because the mechanism to reimburse the Apple watch) – methodologies systematically examined and incrementally carried out throughout all applications over current years – has showcased extraordinary efficacy in partaking members. This, in flip, has the direct causal impact of accelerating the embrace of the specified wholesome behaviors amongst Vitality’s members.[11]

Lively Rewards and Apple Watch profit impacts on the UK portfolios (Supply: Discovery)

Upon analyzing the affect of Lively Rewards on Discovery’s member bodily exercise, members who participated in Lively Rewards noticed greater than a 20% improve in bodily exercise days no matter their well being standing. This improve is observable throughout the whole spectrum of well-being, encompassing people categorized as “wholesome,” “with steady power situation,” “with vital power situation,” and “with advanced power situation.”[12]

An evaluation of the bodily exercise patterns throughout the similar member cohort, each previous to and subsequent to the implementation of those two superior behavioral change methodologies, has yielded notable findings. Following publicity to Lively Rewards, the common exercise stage exhibited a commendable upswing of 18%. Furthermore, with the added incorporation of Apple Watch advantages, this common exercise escalation escalated to a powerful 35%. This enhancement is constantly noticed throughout numerous generational segments, with all age brackets showcasing increments surpassing 20%. Notably, people aged 50 and above displayed a very substantial uptick of 51%.[13] Comparable items of proof have been measured in South African, UK, US, and Australian portfolios.

The better the proportion of engaged members, the upper the affect created on the insurer’s technical outcomes. A Swiss Re’s “Well being and Wellness Engagement Impacts” research analyzing a life insurance coverage conduct change program estimated a threshold of 25% engagement as requisite to make sure a constructive ROI for the insurer. Exceeding 90%[14] of Vitality’s markets with multiple 12 months of maturity have already achieved engagement ranges surpassing this specified threshold amongst members. One of the vital efficient worldwide applications – a mature market – has reached a exceptional 64% engagement[15] charge amongst its members.

The supplied proof undeniably underscores the effectiveness of this strategy—based on expertise and information shared by policyholders—in enhancing the Profitability of the insurance coverage portfolio. This type of direct affect on technical outcomes serves as a major cause for the incorporation of any insurtech methodology throughout the insurance coverage area. Nevertheless, after we embrace my 4Ps framework for evaluating insurtech initiatives a further trio of impacts warrants consideration to focus innovation efforts throughout the insurance coverage sector. These embody Persistency, highlighting elevated retention; Proximity, denoting frequency of interplay with the shopper; and Productiveness, indicating improved prime line.

All Vitality portfolios have constantly demonstrated superior retention charges when contrasted with the broader market. Moreover, the churn ranges noticed inside probably the most engaged members usually vary between one-third and half[16] of these noticed in clusters exhibiting much less wholesome behaviors. This phenomenon exerts an distinctive affect upon the lifetime worth of a policyholder cohort—what actuaries quantify as New Enterprise Worth—leading to a shift within the high quality of the insurance coverage ebook.

The heightened stage of engagement, described within the first a part of the article – undoubtedly amplifies the frequency of interactions (app utilization, push notifications, emails, …) between the insurance coverage provider and the policyholder. A number of of the Vitality life portfolios have encountered a mean above 20 touchpoints per thirty days with policyholders[17], a marked departure from the historically minimal touchpoints related to life portfolios. Noteworthy is a selected Vitality portfolio whereby the utilization of the insurer’s digital channels amongst members has surged greater than fourfold[18] after the introduction of the above-mentioned Lively Rewards.

Considered one of Discovery’s worldwide companions has disclosed the impact on cross-selling: the depend of insurance policies per buyer is fivefold better amongst Vitality members compared to the traditional portfolio.[19] An identical pattern is clear inside an evaluation of Discovery’s policyholder cohort with over 5 years of engagement. The examination reveals that probably the most engaged members preserve a mean of fifty%[20] extra insurance policies in distinction to their much less engaged counterparts. This drive to extend productiveness is the final however not least space of affect.

The gross sales performances are evidently influenced by a mess of things, encompassing the insurer’s technique and initiatives, contingent market situations, and aggressive dynamics. Consequently, attaining a precise quantification of the affect of the Vitality strategy proves to be a formidable problem. However, a plethora of anecdotal proof lends credence to the notion that this side might certainly be certainly one of appreciable significance:

- A life portfolio progress fourfold the market, with market share rank from eleventh to seventh in 4 years (mature nation)[21];

- Well being carriers had a 33%[22] top-line progress over 6 years in contrast with a shrinking market (mature nation);

- A life bancassurance participant elevated market share from 2% to 7% in 4 years (rising financial system)[23].

This detailed overview demonstrates with information and figures the effectiveness of the Vitality mannequin – concretely attaining adoption and engagement among the many complete spectrum of well-being – and the profitable journey in replicating it in all of the geographies.

Following the identification of the underlying causes of claims, this strategy successfully incentivizes policyholders to reveal verified behavioral info, thereby securing rewards. This Shared-value mechanism serves to optimize their ongoing engagement whereas additionally yielding superior outcomes for the insurance coverage enterprise, a portion of which is shared again to the policyholders.

Discovery has meticulously cultivated a collection of specialised competencies, encompassing the adept steerage of behavioral change, adept engagement with policyholders, the skillful orchestration of an ecosystem of retail companions to sustainably ship interesting rewards, and a complete array of supplementary aptitudes required to make sure the seamless integration and alignment of the Vitality strategy throughout actuarial, advertising and marketing, and distribution features. This prowess has been perpetually honed by way of collaboration with worldwide companions and an unwavering dedication to steady innovation.

Evidently, this system utilized to well being and life transcends the scope of a standard wellness program, regardless of bodily exercise constituting a foundational incentivized part over its three-decade trajectory. It signifies an emergent insurance coverage paradigm that holds the potential for extension throughout numerous insurance coverage enterprise traces (in South Africa, Discovery has efficiently utilized it to auto insurance coverage). This extension goals to foster much less dangerous behaviors amongst policyholders and, when deployed inside business traces, extends its affect to embody front-line staff.

Notes

1. Discovery web site, https://www.discovery.co.za/corporate/investor-relations-about-us.

2. Discovery Group unaudited interim outcomes for the six months ended 31 December 2022 (slide 9), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

3. Primarily based on information from the Vitality System Platform.

4. Discovery web site, https://www.discovery.co.za/vitality/join-today/.

5. Discovery Group audited outcomes for the 12 months ended 30 June 2023 (slide 62), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final-fy-2023-update.pdf.

6. Discovery Group audited outcomes for the 12 months ended 30 June 2021 (slide 77), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2021/fy-results-final-2021.pdf.

7. Discovery Group unaudited interim outcomes for the six months ended 31 December 2022 (slide 21), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

8. Discovery Group unaudited interim outcomes for the six months ended 31 December 2022 (slide 10), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

9. The case for getting lively and driving nicely, white paper.

10. Evaluation by Discovery Well being Medical Scheme, 2020.

11. RAND Europe Study: Incentives and physical activity

12. The case for getting lively and driving nicely, white paper.

13. AIA Vitality, Introduction to Lively Advantages and Apple Watch Profit, https://www.aia.com.au/content/dam/au/en/docs/press-releases/2022/apple-watch-insights.pdf.

14. Discovery Group unaudited interim outcomes for the six months ended 31 December 2022 (slide 9), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

15. Discovery Group audited outcomes for the 12 months ended 30 June 2023 (slide 62), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final-fy-2023-update.pdf.

16. Sourced from information from varied Vitality companions.

17. Why well being and wellness initiatives matter for actuaries: John Hancock Vitality as a case research, John Hancock, 2019, https://www.soa.org/globalassets/assets/files/e-business/pd/events/2019/annual-meeting/pd-2019-10-annual-session-041.pdf.

18. Primarily based on Discovery information.

19. Sourced from information from Vitality accomplice.

20. Primarily based on Discovery information.

21. Sourced from information from Vitality accomplice.

22. Vitality accomplice market information in contrast with information from the sixteenth Version of the LaingBuisson Well being Cowl report.

23. Sourced from information from Vitality accomplice.

About The Writer

Matteo Carbone is the founder and director of the IoT Insurance coverage Observatory, co-founder of Archimede Spac, and a world InsurTech thought chief and investor. He’s internationally acknowledged as an insurance coverage trade strategist with a specialization on innovation. Matteo is creator and world-renowned authority on InsurTech – ranked amongst prime worldwide InsurTech Influencers – and he has spoken to audiences in twenty completely different nations. He revealed the primary bestseller devoted to InsurTech: “All of the insurance coverage gamers will likely be insurtech” and is member of the Forbes New York Enterprise Council. Matteo has suggested greater than 100 completely different gamers in ten insurance coverage markets around the globe and has vast insurance coverage expertise which incorporates arrange of commercial and business plans, progress technique definition and help within the start-up of recent initiatives, digital technique improvement, insurance coverage merchandise innovation, channel technique and business mannequin definition, startups mentorship and recommendation M&A offers. He has labored immediately with gamers accounting for greater than 80% of the worldwide IoT insurance coverage volumes (variety of insurance policies on auto telematics, good residence, and linked well being). Earlier than creating the IoT Insurance coverage Observatory and co-founding Archimede, he spent eleven years in Bain & Firm’s Monetary Service follow.

About IoT Insurance coverage Observatory

The IoT Insurance coverage Observatory is a world insurance coverage think-tank which has put collectively executives from greater than 70 insurance coverage teams, establishments and the Web of Issues ecosystem to debate the nice potential of probably the most mature InsurTech pattern, in addition to the challenges it poses to the insurance coverage enterprise. The main target is on any insurance coverage answer primarily based on sensors for gathering information on the state of an insured danger and telematics for distant transmission and administration of the info collected. For extra info, go to iotinsobs.com.

SOURCE: Matteo Carbone

[ad_2]